An IVA; short for Individual Voluntary Arrangement is a formal Insolvency solution designed to help you deal with debts that you cannot afford to repay. An IVA should be considered carefully and researched thoroughly, before you decide if it is right for you.

Below we have provided an extensive list of IVA faqs so that you can gain more knowledge about the solution and how it works. Just click on each question to expand the answer.

If you have any additional questions that are not answered below, or would like advice on an IVA, call us on 0800 043 3328 and we will be happy to help. You can also click here to fill in the form and we will get in touch. All advice is free and confidential and you are under no obligation to proceed with a solution by contacting us.

An IVA is a formal insolvency solution that allows you to deal with *unsecured debts that you cannot afford to repay. In an IVA you agree an affordable repayment plan with your creditors (the people you owe money to), which can be a monthly repayment or a lump sum (if you can gain access to it). You usually pay less than what you owe in an IVA and on completion of the arrangement, any remaining debts are written off.

*Unsecured debt refers to debt that is not secured against an asset or protected by a guarantor. This includes debts such as credit cards, store cards, overdrafts and some loans.

Insolvency is the term given to a person or company that is unable to repay their debts, on time, as agreed by their creditors. There are different types of Insolvency solution available for dealing with debts.

Any business or individual that is struggling with repaying their debts may be eligible for an IVA, however there are certain criteria (see below) where an IVA is better recommended for both you and your creditors over other Insolvency solutions, such as Bankruptcy.

The criteria where an IVA may be favoured over other Insolvency solutions are as follows:

It is not possible to do an IVA on your own. An IVA is a legal debt solution and you will need the assistance of a professional called an Insolvency Practitioner or IP to apply for one. The IP will also supervise and monitor your IVA for its duration. An Insolvency Practitioner is the person qualified and licensed to act on behalf of someone who is Insolvent. Most IP’s are accountants or insolvency specialists. We have a team of 5 IP’s at McCambridge Duffy, which allows us to handle all Insolvency proceedings in house.

There is no clear answer for this. It really depends on your financial situation and your own choice of which you feel is right for you. IVAs and Bankruptcy are two very different Insolvency procedures that can both deal with your debts. They also have some similarities. Knowing which is better for you is dependent on your circumstances. Certain factors of each Insolvency solution will affect you differently. For example:

There are also certain factors in both solutions that are similar. For example,

Debts that can be included in an IVA are:

Debts that cannot be included in an IVA are:

A standard IVA usually lasts for 5 years (60 monthly payments), although it can be completed in as little as 12 months if you can propose a lump sum payment to settle your debts.

If you are a homeowner with equity, this will be reviewed in the final year of your IVA. You may be required to introduce some of your share of the equity into the agreement. If this is not possible then your IVA could be extended for up to another year. This will all be explained in detail prior to applying for an IVA.

Pros of an IVA

Cons of an IVA

No two IVAs are the same. Your monthly IVA payment is completely unique to your circumstances. It is calculated by analysing your living situation, household income, household expenses, your priority debts and your unsecured debts. The money left over each month after all expenses and priority debts (but not including other debt repayments) are paid will be your IVA payment.

Yes. It is important that your IVA payments are sustainable and affordable. You are entitled to a reasonable budget for living and your debt advisor will use recommmended guidelines that cover every aspect of expenditure to ensure that you have enough money to live on each month. They will discuss all of this with you to make sure that you are happy with the suggested amounts for your living expenses.

The fees payable in an IVA come from your monthly payment. Fees are agreed with the creditors who set our fees at the beginning of the arrangement. You will never receive a bill from us. So essentially, the fees and costs for an IVA all come from the one monthly payment that you make each month.

At McCambridge Duffy, we do not charge upfront fees for drafting and submitting your IVA Proposal. We only put an IVA case forward if we believe it will be a successful one for both you and your creditors. In the event that your IVA proposal is unsuccessful, then you will not be charged a penny.

If you cannot pay your debts as they fall due, you are insolvent; by law your alternatives are debt management, bankruptcy, a Debt Relief Order, an Individual Voluntary Arrangement or some other debt solution.

An IVA will be a viable option if

Deciding if an IVA is the right choice for you is not something that should be entered into lightly or hastily. It is important that you find out and digest as much information as possible to determine if it is your best option. You also need to make sure you have discussed all possible alternative options with your debt adviser or IP. Essentially, we can only advise and provide all the information. It is you that has the final decision on whether or not you want to proceed with the application.

We cannot speak for all Insolvency firms that are handling your IVA proposal, but here at McCambridge Duffy we have a very high IVA acceptance rate. Because we do not charge any upfront fees, we only put forward an IVA proposal if we believe it will be a successful one for both you and your creditors. If your IVA proposal is unsuccessful, then you will not be charged a penny from us. Be wary of Insolvency firms that are charging upfront fees for putting through your IVA proposal. If your IVA is not accepted, you will be out of pocket for the money that you have paid up front.

Most creditors are fully aware of an IVA and what it is, as it's been in existence for over twenty years. If 75% of your creditors by debt value vote in favour of your IVA, then all creditors are bound by its terms. Creditors can suggest alterations to your proposal and you can choose whether to accept them or not. If your creditors vote against your proposal you still have the option of an informal arrangement or other solutions.

Generally speaking, creditors favour IVA’s over some other Insolvency solutions as it shows you have a willingness to try and pay back what you can and gives them a return on their money outstanding.

An IVA must be approved by more than 75% (by debt value) of your creditors at a meeting of creditors. On some occasions creditors may reject a proposed IVA. The most common cause is that they are not happy with the proposed arrangement and it is not at a level that meets individual creditor guidelines.

If your IVA proposal is rejected at Meeting of Creditors, it may be possible for your IP to make amendments and re-propose the IVA if you are in a position to offer a revised IVA payment. If this is not the case, you will have other options available to deal with your finances. We can discuss this with you further. Call 0800 043 3328 for more information or click here to read more about rejected IVAs.

It is only natural to wonder how a formal Insolvency procedure such as an IVA will affect your partner or spouse. If the debts are your own then your partner, their income and their assets will not be affected. If you are co-habiting you may need to disclose your partners income, but this is simply to analyse how the household income and expenses work and to make sure the bills are being paid fairly and evenly between both of you.

Your partner will be affected if you both have joint debts. You are both responsible for the full amount of the debt. An interlocking or joint IVA would be recommended in this instance, if possible, because if you go into a single IVA, then your partner is still responsible for paying the joint debt regardless.

Yes. Your credit rating is affected in an IVA. It will be noted on your credit file that you are in an IVA and your credit rating will be affected for up to 6 years. However, bear in mind that if you are struggling to repay your debts before seeking help and you have missed payments, then chances are your credit rating is already affected and will continue to deteriorate. The consequences of not addressing your debt problem could be just as harmful to your credit rating. Any debt solution you enter into will affect your credit rating because you are no longer paying your agreed contractual repayments with your creditor.

After the 6 year time period of your credit rating being affected, you credit rating will start to repair.

When you are in an IVA all of your current credit agreements will be stopped. You are not permitted to obtain any new credit until after your IVA is complete.

You can have a bank account in an IVA. In some cases, you may be required to change bank accounts, while your IVA is being prepared. This is because if the bank involved is also a creditor involved in your IVA, they may attempt to remove money from your account for any debt outstanding. A new bank account with a creditor that you have no debts outstanding with, will prevent any issues like this. We can let you know if any of your creditors are linked to your current bank account.

Before you begin an IVA your IP will discuss everything you need to know about what can happen to your home or mortgage when in the arrangement.

In an IVA your home is protected. You do not have to sell your home. However, if you do have equity in your home after taking account of the mortgage on it, you will likely have to release part of your share of the equity by means of a remortgage, in the final year of the arrangement. If you are unable to remortgage or it is not affordable to remortgage at this stage, you may have to continue making IVA payments instead, for up to another year.

If you are looking for a home while in an IVA, it is not likely that you will be able to obtain a mortgage.

As a general rule, your assets are protected in an IVA. You should make your IP aware of any assets that you have such as property, vehicles or other items of significant value. If you own a car you are usually able to keep it, depending on it’s value. If your car is deemed as excessive in value, your creditors might consider this as a problem and ask you to sell it. If you have to sell your car, you will be allowed to buy a replacement of a lower value. If you own multiple cars, this is something that might also be queried.

If you do not own a car, but have a car out on Hire Purchase it is likely that you will be able to continue paying for this. Some HP companies won’t allow this, so you will need to check that this is allowed with your HP Company. When the HP payments finish, you may be required to contribute the extra money towards your IVA.

State Pension

If you enter an IVA your state pension is not affected.

Personal Pension

Any money already paid into your pension is safe. But any current/ future pension payments could be affected in an IVA. Creditors might require you to cease pension payments for the duration of your IVA and contribute the payments instead towards your monthly IVA payment. If creditors do not require you to cease pension payments, then they might ask for reduced pension payments instead.

If you are to receive a pension lump sum during the term of your IVA, this could be classed as a windfall and you may be required to pay this into your IVA. Your IP can advise further about this.

No, but you do need a source of income or benefits that is more than you need for living expenses.

Generally your job will not be affected in an IVA, but there are some professions where doing an IVA will mean you can no longer practise in that profession, or you will be able to practise but with certain restrictions. i.e. if you are in a role related to finance, law, property or accountancy. If you are worried about how an IVA might affect your job, you could check the conditions of your contract to make sure.

McCambridge Duffy offers a complete guarantee of confidentiality and privacy in relation to your financial affairs. We will never disclose any information about you to any outside organisation and will never say who we are when we call you. This means that you can feel safe in providing your contact information, without worrying that others will find out that you are seeking our help.

Generally the only people interested in knowing about your IVA are the people involved in it, such as your creditors and your IP and sometimes utility providers or the local council (if one of your debts is Council tax arrears).

Anyone that does an IVA has their details put onto a public register call the Insolvency Register which is located on the Insolvency website. The website can legally be accessed by anyone, but it is highly unlikely that anyone will check it. It is generally only of interest to people dealing with Insolvency related matters or creditors and credit agencies. Unlike Bankruptcy, your name is NOT published in any local newspaper when you enter into an IVA. This is one of the reasons why an IVA is favoured over Bankruptcy. It is more private.

Approved IVAs are published in Stubbs Gazette, a magazing that can be requested by various Insolvency and financial professionals.

The Insolvency Register is a public register available online. It contains searchable information on any Insolvency solution, such as Bankruptcy, IVA’s and Debt Relief Orders. Anyone who is currently in one of these solutions will have their details on this register. When your Insolvency solution is complete your details will be removed from the register (this can take a few months).

It is important that you keep up repayments on your IVA as failure to do so could result in failure of your IVA and may lead to Bankruptcy. In saying that, an IVA lasts for a significant length of time, so it isn’t uncommon for the odd problem to arise throughout its term, causing you to miss a payment.

If you are worried that you are going to miss a payment you need to contact your supervisor immediately. There may be options open to you, such as a payment break if your missed payment is deemed as an emergency, or you might need your IVA payments temporarily altered. Any missed payments will need to be accounted for and will most likely be added at the end of your IVA.

If you have had a significant change in circumstances during your IVA, your IP may need to negotiate amendments to your IVA with your creditors. If your creditors won’t agree to the amended terms then your IVA could fail, which could lead to Bankruptcy.

If there is a valid reason a payment break can be arranged with your supervisor or IP. This will in turn cause your IVA to be extended as the missed payments will likely need to be added on at the end of your IVA.

You can cancel an IVA but it is not advised unless the reasons for doing so are acceptable. Cancelling an IVA can result in serious consequences. It needs a lot of thought and you should discuss it and your reasons why you want to cancel with your IP or supervisor.

If after discussing with your IP you want to cancel, then you need state this to your IP in writing. Your IP will fail the IVA and send you a notice of termination. You will still need to address your outstanding debts and be responsible for IP fees. If you do not sort out your debts with your creditors promptly after termination, you could be made bankrupt.

How your IVA fails is dependent on the terms of the arrangement, how much has been paid into the arrangement and at what point it fails. Some IVAs will require your IP to apply to the court to make you bankrupt if enough contributions have been made to meet the costs associated with this process. Other IVAs will simply fail and a payment will be made to creditors if possible.

Any money already paid into the arrangement will be used to meet the fees and costs associated with its preparation and supervision, to fund a bankruptcy petition (if necessary) and / or will be distributed to creditors.

You will lose the formal protection of an IVA when it fails and creditors can therefore instigate recovery action against you. They can apply interest and charges to your accounts.

In an IVA, your supervisor will carry out yearly reviews of your income and expenses to ensure that your monthly payments reflect your surplus income. Your IVA payments could go up or down a little depending on the review. If your income increases significantly during the term of your IVA, you may have to contribute more to the monthly payments.

If you receive a large sum of money during the term of your IVA, such as a lottery win, a work bonus, or inheritance, this is considered as a windfall. Such a payment will have to be declared to your IP and paid or part paid into the IVA for the benefit of the creditors. This also includes PPI refunds.

On completion of your IVA you will receive your completion certificate. Any remaining debts are written off as agreed and you can start over free of debt. Your creditors will update your credit file. Keep an eye on your credit report in the following months to make sure everything has been updated by your creditors.

Your credit rating will begin to repair 6 years after the commencement of your IVA.

Yes. A CCJ can be included in an IVA. Inform us about this when you chat to us. The IVA can prevent any further action being taken.

Yes, you can. A Guarantor Loan can be a loan which you have taken out and which has been guaranteed by another person or a loan taken out by another person and guaranteed by you. If you have given a Personal Guarantee (PG) for a loan taken out by another person (your partner, spouse, sibling, child, parent or indeed any related person or any third party), you can still enter into an IVA. However, the PG has to be disclosed in the IVA proposal. If the loan hasn’t been called in (that is, if the creditor hasn’t demanded that the loan be repaid immediately), then the amount usually entered as a debt in the IVA proposal is just £1. If the loan has been called in, the full amount of the debt has to be entered in the IVA. Similarly, if the debt is called in during the term of the IVA, then again the whole of the outstanding debt becomes one of the IVA debts. If it is not called in during the term of the IVA, then your PG no longer applies and you will no longer be responsible for the payment of the debt after the successful completion of your IVA.

Please note also that if another person has given a personal guarantee for a loan that you have taken out, then the full amount of that loan has to be included in your IVA proposal. The lender can of course pursue the person who gave the PG on your loan for any shortfall that arises because of your IVA. Indeed, as soon as the first default occurs on such a loan (for example when a scheduled contractual repayment is missed), the creditor can immediately pursue the guarantor for the full amount outstanding.

There is no statutory minimum level of debt that you need to have to qualify for an IVA. However, in practice most IVAs will have upwards of a total of £10,000 debts although some IVAs may have total debts of as low as £5,000. Bear in mind that you cannot be bankrupted unless one of your debts amount to at least £5,000. Also, you should be aware that an alternative insolvency solution is available in the form of a Debt Relief Order (DRO) if you have a low level of debt, low disposable income and few assets.

Yes, it does. Of course, if you have financial difficulties such as having defaulted on repayments of your loans, then your credit rating may be already affected even before you enter into an IVA. Assuming that you have a normal credit rating when your IVA commences, then the event of your IVA will trigger negative credit ratings on all your debts in the IVA. This negative credit rating will continue for six years from commencement of your IVA and only after that time has elapsed will your credit rating return to normal. You may have to be pro-active in getting the defaults removed from your credit files after the six years have elapsed.

Yes, you can. It depends on the circumstances of your financial relationship such as if you have joint debts, joint mortgage and how your ordinary living expenses are split up between you and your partner. It would be unusual to not divulge to your partner that you were planning to enter into an IVA since much of the information that is needed to be disclosed to your creditors in your IVA might involve your partner’s income, any joint assets you might have and your domestic arrangements for payment of living expenses. However, in certain circumstances, it would be possible to keep your partner from knowing about your IVA, particularly if you have been keeping your financial arrangements completely separate from each other.

If you want to consider entering into an IVA, the first thing to do is to choose a firm which offers insolvency services such as IVAs. If you have access to the internet you will find the names of many companies offering such services and you probably want to choose a firm which does not charge up-front fees for initial advice or which perhaps charges a small nominal or perhaps refundable fee (in the event that you decide not to proceed). Once you contact an insolvency services firm, you will usually be taken through the various steps in the process. This process involves you providing financial information regarding your debts, your assets (such as house and/or car) your earnings and so on. Your circumstances can usually assessed quite quickly and a preliminary advice be provided as to whether you may be suitable for an IVA. You can of course pull out of the process at any time but if you stick with it, you can have an IVA proposal ready to be presented to your creditors within a short number of weeks, depending of course on the complexity of your circumstances. The next stage is that a Meeting of Creditors is arranged and if your creditors accept your proposal, you can enter into an IVA with them.

Yes, you can. Your previous IVA may have been successfully completed or it may have failed during the term of that IVA through no fault of your own. In either case, you can still offer proposals to your creditors for a second IVA if your circumstances have changed significantly since your first IVA completed. Clearly, creditors and your IP will have to be satisfied with your new IVA proposals and you will have to demonstrate that your new IVA is genuine, credible and sustainable.

No, not necessarily. To enter an IVA, you have to be insolvent but if your partner is not insolvent then his or her details do not have to be included in the information that you provide to your creditors. However, if you jointly own assets such as a house or vehicle(s) or if you have joint debts or you each pay a portion of your mortgage or house rental payments or if you share the payment of normal living expenses then your proposal for an IVA has to take account of how each of these matters is dealt with. It may be necessary to disclose what your partner’s wages are so that creditors can judge and ascertain for themselves whether you and your partner each pay their fair share of such costs and living expenses, usually in proportion to your respective earnings. It would be quite standard to disclose to your creditors what your partner earns so that they can assess for themselves that your IVA proposal is reasonable and sustainable. In any case, your partner has full control of his or her wages but it may be necessary for the amount of those wages to be disclosed simply to ensure that living expenses are shared fairly as between you and your partner.

Yes, you can. Your previous IVA may have failed through no fault of your own if for example you became unemployed and were unable to continue making payments into your IVA. Creditors may have been unwilling to grant you sufficient payments breaks until you were able to secure new employment. If your financial circumstances have now improved to the extent that you can sustain payments into an IVA, creditors may accept your proposals for a new IVA. Your insolvency practitioner can advise you in this regard.

You still have full control of your wages. They are paid into your bank account in the normal way and you have full control over all payments out of that account. Even if you are paid in cash, you still have full control of your income. However you need to fully comply with your IVA supervisor in disclosing what you are earning. If your net earnings increase over time, your supervisor will be obliged to require you to contribute a portion of any extra earnings into your IVA for the benefit of creditors. This is spelled out quite clearly in your IVA proposal which you and your creditors have agreed. Reviews of your income are usually carried out annually by your IVA supervisor when you are in an IVA.

Yes, you can. The only difference between a PAYE worker and a self-employed person as far as an IVA is concerned is that a self-employed person needs to ensure their your tax returns are made in a timely way and kept up to date during the term of their IVA. It is also important that before you enter an IVA, your tax returns are up to date. If you owe monies to HMRC, then they can vote to accept or reject your IVA proposal like any other creditor. Your insolvency practitioner will fully advise you in regard to these matters so as to give your IVA proposal the best chance of being accepted by your creditors.

Most people who enter into an IVA do not lose their house. A well-constructed IVA proposal will deal with your house so as to give you the best chance of retaining it. You will have to keep up your contractual mortgage payments during the term of your IVA and if you do so, you will not lose your house. This is one of the great attributes of an IVA in so far as the debtor can deal with their unsecured debts in the IVA and still hold onto their house. There is a much greater chance of losing your house if you enter bankruptcy than if you enter an IVA.

Before you enter an IVA, all your financial circumstances are examined and this includes all bank accounts you have. In order to prepare your IVA proposal, your insolvency practitioner will require copies of your bank statements so as to have a complete, truthful and accurate picture of your finances. After you enter the IVA, you would not normally be required to provide bank statements on an ongoing basis to your IVA supervisor. Provided you comply with the terms and conditions of your IVA and are truthful with your supervisor then regular examination of your bank account would not normally be required. Since you are prohibited from obtaining credit in excess of £500 during the term of your IVA except with the express permission of your IVA supervisor on behalf of your creditors then there is usually no need to check you bank accounts in this way.

Technically yes, but the term ‘joint IVA’ is meaningless as there is no such thing. This type of IVA is referred to as ‘interlocking IVAs’. Interlocking IVAs are where a couple wish to put forward IVA proposals for IVAs where both parties are insolvent.

No, you cannot obtain further credit such as a loan, except in exceptional circumstances and then only with the express permission of your IVA supervisor and your creditors. Your IVA proposal may allow you to have a certain amount of credit relating to, for example, some of your utility accounts but then the upper limit of such credit is £500. It is possible that an unusual event occurs which necessitates some borrowing by you but you may not proceed to borrow any further money without the express permission of your IVA supervisor and your creditors. Failure to comply with this is likely to lead to failure of your IVA.

No, not necessarily. Your IVA proposal may be based on your releasing funds into your IVA by for example selling your property and contributing the net proceeds (or a large proportion of these) into your IVA. Alternatively you may have a lump sum available to contribute into your IVA or you may be able to offer a third party lump sum contribution into your IVA or your partner who is not insolvent may be agreeable to make regular contributions into your IVA. If your only source of income is for example social welfare benefits or illness benefit, it is unlikely to offer sufficient surplus income to give creditors a reasonable return in your IVA. Your insolvency practitioner can usually quite quickly assess if your income or lump sum offer is sufficient to adequately fund an IVA to the satisfaction of your creditors.

While there is no legal bar on somebody obtaining a mortgage whilst in an IVA, in practice it could pose difficulties. Firstly you would have to obtain the express permission of your IVA supervisor and that of your creditors, since obtaining a mortgage involves taking out more credit. However, if it is in the interest of your creditors, it may be possible to obtain their permission. In the current financial climate, it is likely that you would need a deposit (since 100% mortgages are largely a thing of the past) and where would you get the deposit funds? How would you make the monthly mortgage payments if all of your surplus income (or most of it) is already being paid into the IVA? However, there could be exceptional circumstances where it would be in the creditors’ interest that you take out a mortgage or indeed that you re-mortgage your existing mortgaged property by extending the term of the mortgage and by releasing equity for the benefit of creditors and thereby ending your IVA early. If for example you are currently renting and paying exorbitant rent, then a mortgage might be cheaper than renting. You may be able to get assistance from a housing association who might enter into a mortgage/rent agreement with you, again for the benefit of creditors. Bear in mind that commercial mortgage lenders would be likely to charge premium interest rates given that you are a credit risk and are already in an IVA, a fact that you would have to disclose to them.

When you enter into an IVA, the IVA proposal as agreed between you and your creditors usually provides for regular reviews of your income (at least annually but sometimes more frequently) and for a portion of any additional earned income to be contributed to your IVA. The amount is generally of the order of 50% of any additional earned income over and above a certain amount. The IVA proposal usually spells out how the amount is calculated. So, the answer is yes, you may be asked to pay more into your IVA but only if you earn more money above certain thresholds.

It is worth considering the restrictions that apply before you enter an IVA. Certain professions and occupations have sanctions which may be or indeed must be applied if you enter an IVA (or indeed any other financial arrangement) with your creditors. You should check the terms and conditions of your employment to see if there are any sanctions which cause you to lose your employment or be restricted from advancement or promotion in your employment if you enter an IVA. If you are a director of a company or are self-employed in your own company the articles of association may have sanctions which may adversely affect your employment or may require you to resign your directorship if you enter an IVA.

You may also be a member of a recognized professional body which prohibits members from entering an IVA on pain of losing their membership of that body. There may also be other less severe sanctions applied by your employer or professional body. After you enter an IVA, the main restrictions that apply relate to the taking out of credit or obtaining loans in excess of £500. These are normally prohibited except by express permission of the IVA supervisor and your creditors. Other matters to bear in mind are that your lifestyle may be somewhat restricted in that you need to live within the constraints imposed by the IVA proposal relating to expenditure.

You need to supply the following paperwork that applies to you:

These documents are needed in order to prepare the IVA. During the term of the IVA, if approved by creditors, some of the documents will have to be updated and provided at least annually (e.g. payslips).

It may be possible to exclude debts to your employer in your IVA proposal but otherwise you cannot refuse to disclose all of your debts. This is to ensure that all creditors are treated fairly and equally in the course of your IVA. However, certain debts or outgoings must be paid in full during the course of the IVA (e.g. fines, child support, HP payments or mortgage payments) and such debts are excluded in the sense that the relevant creditors do not receive a dividend from your contributions to the IVA but are paid in full by you directly during the term of the IVA.

This needs to be disclosed to your IVA supervisor as well as any overtime payments, bonuses or commission payments. The supervisor will calculate how much of any such additional earnings must be contributed to the IVA. The IVA agreement itself spells out how this works and it seeks to be fair in that a certain amount can be retained by the debtor. Any increases in costs of living and inflation are taken into account as are any extraordinary or additional expenses that are being incurred. Usually these matters are dealt with at the annual review of the IVA.

No. To apply for an IVA, you have to engage the services of a qualified insolvency practitioner who is licenced and regulated by a professional body (of which there are a number in the UK). At the end of the day the IVA proposal is made by the debtor but the proposal is fully vetted by the insolvency practitioner to ensure that it is complete and complies with the statutory requirements. The debtor should satisfy himself or herself that all relevant matters are disclosed truthfully in the proposal.

No, it does not. A certain amount of your income is allowed to be retained which can be put aside by the debtor for ‘a rainy day’. It is usually listed under the term ‘Contingencies and Emergencies’.

An IVA can be set up within a few weeks of you contacting the firm providing insolvency services – anything from three to six weeks. It does depend to some extent on the complexity of your financial circumstances. However, if the debtor provides the documents and information promptly when requested, it is not unusual for the Meeting of Creditors to be scheduled in the same month as when that initial contact took place. It is remarkable how the lapse times for preparations of IVAs has shrunken in the last few years.

The vast majority of IVAs are scheduled to last for five years. However, the duration can be as short as six months where for example the proposal is for the payment of a lump sum with either no or few monthly contributions into the IVA. Some IVAs may last for more than five years. This usually occurs where the debtor was granted payment breaks and the extra time is added on at the end to make up for the months of missed payment. It would be unusual to have an IVA that lasted more than seven years. Some IVAs are set up initially to last up to six or seven years but these are rare occurrences.

Not necessarily. If you choose not to disclose to your parents that you have some financial difficulties, then there is no need for them to be aware that you are in an IVA. They may of course be assisting you either consciously (if you have told them about your IVA) or unconsciously (if they are unaware about your IVA) by for example allowing you to live with them rent-free or at a reduced cost or perhaps by covering part of the costs of your living expenses. There is always a risk that they become aware of the IVA accidentally if you left some documents or mail relating to the IVA lying about or if they should accidentally overhear you discussing the matter on the phone. However, there is no need for them to become aware of it otherwise and it should not affect them.

For six years from commencement of your IVA. It should be removed automatically when that time has elapsed. If it still remains on your credit file after that time has elapsed, you may need to proactively seek its removal by contacting the relevant credit reference agencies yourself.

Absolutely not. Your bank account may not be accessed by any third party which includes the insolvency practitioner who is supervising your IVA as well as his or her staff. However, if your bank is a creditor in your IVA, then it is likely that your account could be frozen once your bank becomes aware that you are applying for an IVA. If you have more than one account with the same bank and if any of those accounts is in credit (I.e. if you have funds saved therein), then the bank may have ‘offset’ powers enabling it to use the amount that is in credit to reduce the debt that you owe to them in relation to other accounts that may be overdrawn or ‘in debit’. When setting up your IVA proposal, you should disclose all your accounts to your insolvency practitioner who will advise you as to how you should proceed.

No not necessarily. If you simply have a current account with a particular bank and the account is in credit and there is no overdraft facility above the £500 limit on the account and if you have no other accounts with borrowings from that particular bank then you may not need to change banks. Generally however, it is necessary to change banks since many people have more than one account with their preferred bank and if any of those accounts is overdrawn or is a loan account then it makes sense to change to a different bank and set up a current account without any overdraft facility greater than £500 with their new bank. That new current account will be the one into which you will have to arrange to have your wages, salary, benefits and other income streams paid. You will also need to move any direct debits you may have to that new bank account.

You do have to disclose to your insolvency practitioner if you have any savings when your IVA proposal is being prepared. You may be allowed to retain a small amount of those savings to be used for contingencies that may arise during the course of your IVA. Once your IVA is up and running, you are allowed to save any funds which you accrue by for example keeping your expenditure below the allowable living expenses which are spelt out in the income and expenditure part of your proposal. In an IVA, you are allowed to retain a certain portion of any overtime, bonuses or commission that you earn under the 10% 50/50 rule, and provided you have accounted to your IVA supervisor for what is due to be contributed into the IVA it is entirely up to you what you do with any savings you are able to accrue in this way.

Many self-employed people with their own businesses enter IVAs to enable them to deal with their personal insolvency. Assuming that their business is their main source of income and that it is a viable business properly managed with its tax affairs in order then there is no reason why it should be adversely affected by the IVA. Your insolvency practitioner will tease out any issues that might arise with the business. For example if you have given personal guarantees in relation to any borrowings that the business has, then such liabilities would have to be included in your IVA proposal. The other main consideration is the ownership and value of the business. There is also a risk that trade creditors who supply the business may become aware of the IVA and decide to tighten up on any credit facilities they provide to the business. In preparing any IVA proposal all of these matters need to be considered in the context of the nature of the particular business.

The monthly amount that you will have to pay will depend on how much surplus income you have remaining after account is taken of your reasonable living expenses and those of your dependants (if you have any) and allowance is made for your monthly mortgage payments (or the rental costs of your accommodation) and for any other allowable outgoings you have such as child support payments and any special living costs such as special dietary requirements. Clearly the monthly amount you have to pay into your IVA can vary hugely – it could be as little as £100 and there is really no upper limit. The more you earn, the more you will have to pay. Generally most IVAs have monthly contributions between £200 and £600 per month. Of course some IVAs are based on lump sum contributions from the debtor or a third party instead of or supplemented by monthly contributions and in such cases the monthly contributions, if any, can be quite low and/or the term of the IVA can be quite short – perhaps one or two years. Your insolvency practitioner will calculate what you can reasonably afford to pay.

Yes – if your surplus income is low. However, the fees and outlays of your insolvency practitioner will have to come out of your monthly payments and there needs to be sufficient funds left to pay a reasonable dividend to your creditors. If your proposal allows for the payment of a lump sum from a third party or from your own funds, then the monthly payment can be quite low or even zero in some cases. Your insolvency practitioner will advise as to what the monthly amount is likely to be.

If your partner is solvent and able to meet his or her liabilities as they fall due then they do not need to enter into an IVA themselves. If you enter an IVA yourself, your IVA will not affect your partner’s house. Your IVA proposal will have to provide some detail in regard to your living expenses including how much rental you pay to your partner for accommodation in his or her house. The normal way of setting out your income and expenditure details is to assign living expenses in the same ratio as the income of each partner. For example, if you earn a net £2,000 per month and your partner earns a net £1,000 then you would normally pay two thirds of living expenses and your partner one third. When both partners have approximately the same net income then living expenses are usually split 50%/50%. The IVA cannot seek to ‘grab’ any part of your partner’s house.

Unless the CCJ becomes secured against your property it will be included in your IVA. In other words the amount of the debt remaining to be paid at the time of approval of the IVA is entered into the IVA as a debt and a dividend will be paid in respect of that debt on an equal footing as the other unsecured debts. One little complication that arises is that if the CCJ debt was being paid by way of an attachment of earnings, it may take up to three months for the court to cancel the attachment of earnings but when that happens, the debt remaining is entered into the IVA and receives a dividend from the IVA at the same rate as the other unsecured debts.

You are normally allowed to retain certain assets while in an IVA. These include tools of trade (i.e. tools which you require to carry on in your normal course of employment), a vehicle of reasonable value, your principal private residence and normal house contents such as TV, furniture & fittings, appliances and so on. Your IVA proposal will detail how you will pay your mortgage on an ongoing basis but if there is equity in your house, there may need to be provision made for release of some of that equity before the end of the term of the arrangement releasing the equity by way of re-mortgage, often required in the fourth year. The released equity is then contributed to the IVA for the benefit of your creditors. If your vehicle is very valuable, you may be required to trade down i.e. to sell your vehicle and to purchase one with a more modest value. The difference in values is then paid into the arrangement. Of course, your IVA proposal may itself provide for the sale of any of your assets including your residence and for a portion of the monies realised to be contributed to the IVA but you will have already agreed to this before your proposal is put to your creditors. Your insolvency practitioner will advise you on all these matters before your IVA proposal is sent to your creditors.

Yes, you can. Before your IVA proposal is sent to your creditors and the Meeting of Creditors is called you can ask your insolvency practitioner to halt proceedings if you do not wish to proceed. In this case, everything goes back to the way it was and creditors are free to pursue you again for the payment of your debts. If the Meeting of Creditors has been arranged and you do not wish to proceed then you can cancel the meeting by so informing your insolvency practitioner. Your IVA proposal will in this case be deemed to have been rejected and again creditors can pursue you for payment of your debts. If your IVA is accepted at the Meeting of Creditors and it is up and running and you then decide to cancel it, your IVA will be deemed to have failed. Again, creditors can pursue you for the payment of debts and there may even be a requirement for the insolvency practitioner to petition for your bankruptcy.

No, any refund of PPI or Payment Protection Insurance to which you are deemed to be entitled (due to mis-selling of the product to you or for any other reason) is not considered to be income. Rather it is classed as an asset and your insolvency practitioner is obliged to recover these funds and to contribute them (less any costs incurred in recovering the refund) into your arrangement for the benefit of creditors. You will still be obliged to continue making your scheduled monthly contributions to your IVA and pay any other lump sums that you may have offered in your proposal.

Generally you will have to change banks before you enter into an IVA. The one exception is that if you have a single current account with your bank with no overdraft facility greater than £500 and no other loan accounts with that bank, you may be able to keep that bank account for use during your IVA (for lodging your wages or salary and for payments of direct debits for utilities and similar payments). Otherwise it is advisable to close all accounts with your current bank and open a current account with a new bank with no overdraft facility greater than £500 and issue instructions to your employer for payment of your wages or salary into that new account. You should also arrange for relevant direct debits to be made from your new bank account.

No, there is no necessity to inform your employer that you are in an IVA and it is unlikely that your employer will discover this unless they do a credit search on you. If they do a credit search, your credit files will carry the information regarding your IVA. One word of caution: the terms and conditions of your employment and of your membership of any professional body may include sanctions which can be activated in the event of your entering an IVA or indeed any other financial arrangement with your creditors or bankruptcy. Before entering an IVA, you should satisfy yourself in regard to these matters, particularly if one of the sanctions is a possible loss of employment, curtailment of promotion opportunities or expulsion or suspension from a professional body (which may be a necessary requirement for your work).

Yes, you can. Your partner may be a stay at home mother or father looking after children - yours or hers/his or both – or may be incapable of work due to a disability or other reason or may be seeking employment or may have independent means and so on. There is no impediment to your entering an IVA just because your partner doesn’t work.

Yes, you can. However, you need to check whether you own assets (such as a house) jointly or if you have joint debts or if your partner may also be insolvent, and how you split up living expenses between you and so on. Clearly if you split up living expenses fairly between you (usually in the same ratio as your respective incomes), and the mortgage or rental accommodation costs are also fairly split and you have no joint debts and you own no assets jointly and you generally keep your finances separate, then you can certainly do an IVA without the participation of your partner. Your insolvency practitioner will be able to advise you more precisely when he or she has established the facts of your situation.

Many insolvency practitioners and the firms in which they are engaged charge no up-front fees for initial advice relating to IVAs or they may charge a small refundable fee which is generally refunded if the debtor withdraws from the process before the Meeting of Creditors is called or if the IVA is not accepted by creditors at the Meeting of Creditors. Generally the fees and outlays of the insolvency practitioner are recovered after the IVA is accepted from the monthly contributions of the debtor to his or her IVA. The fees and outlays have to be approved by creditors at the Meeting of Creditors, where they sometimes reduce such fees and outlays. The debtor is fully aware of what such fees are before the IVA is approved and that these fees will come from their monthly contributions in a gradual way over the term of the IVA.

Yes we are. We are one of the UK’s leading and longest established IVA providers and have thousands of happy clients. We also have one of the highest success rates in the industry. We have 4 full time highly regulated Insolvency Practitioners with a wealth of experience and knowledge which means we can handle everything efficiently in-house.

Yes, McCambridge Duffy and its members are regulated by ICAS (Institute of Chartered Accountants of Scotland) and DETI (Department of Enterprise, Trade and Investment). We are also members of: R3 (The Association of Business Recovery Professionals) and the IPA (Insolvency Practitioners Association).

Simply complete our online IVA application form. We will then get in touch with you to review your current circumstances and advise whether an IVA is indeed the most appropriate solution to your problems. Once we receive your application form, we will either confirm if an IVA is an appropriate solution or offer alternatives. If you wish to pursue the IVA option, we will proceed with your IVA proposal. We will then submit your proposal to your creditors which explains in detail the circumstances of your current problems and your proposal to repay what you can afford. Once creditors accept it, the proposal is sent to you for review. If you're happy with everything you sign the proposal and we will put your IVA in place. At no time throughout this whole process (which can be as little as 4 weeks) do you pay any monies over to us.

" McCambridge Duffy have been great, completely open, honest and non-judgemental from the first phone call. Kept me fully informed through every stage, always did exactly what they said they would and always got back to me promptly. Fully recommended."

Work out what your new monthly IVA repayment could be by filling in our debt and budget calculator form.

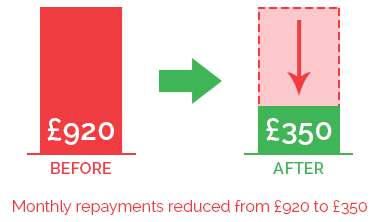

In the IVA example pictured above, our client was struggling with payments of £600 per month to their creditors. We were able to reduce the payment to £240 per month. After 60 months of paying this reduced amount, their IVA will be complete. Any remaining debts will be written off and they will be able to start over debt free.

Chat with one of our debt advisors. We are available to answer any of your questions.

© 2021 McCambridge Duffy Insolvency Practitioners.

All rights reserved

McCambridge Duffy LLP is a Limited Liability Partnership

registered in England and Wales.

Registered number OC309544

Registered office 17 Hanover Square, Mayfair,

London, W1s 1HT