(1) At any time when an application under section 253 for an interim order is pending, the court may stay any action, execution or other legal process against the property or person of the debtor.

(2) Any court which proceedings are pending against an individual may, on proof that an application under that section has been made in respect of that individual , either stay the proceedings or allow them to continue on such terms as it thinks fit.

Note: It is possible that more than one scenario can arise in a case.

Interim Charging Order comes to light at the drafting of the proposal stage & the Court Department applies to court for an Interim Order to protect the debtor from creditor action.

ICO IO MOC FCO HEARING

![]()

NOMINEE MOCD SUPS

FILE REACHES MEETING OF CREDITORS’ DEPARTMENT

FILE REACHES SUPERVISION

Interim Charging Order comes to light whilst case is with the Meeting of Creditors’ Department and is awaiting the creditors’ meeting.

ICO IO(?) MOC FCO HEARING

![]()

NOMINEE MOCD SUPS

FILE REACHES SUPERVISION

Final Charging Order is granted in error prior to Meeting of Creditors taking place. Interim Order in place to freeze creditor action.

ICO IO(?) FCO MOC

![]()

NOMINEE MOCD SUPS

If No – Final Charging Order cannot be challenged. This will impact on the proposal.

If yes – Wait until IVA is approved and then MOCD write to the Court and the solicitor acting for the creditor enclosing copy Chairman’s Report, copy Interim Order and request that Final Charging Order be removed (use MOCD Scenario 3 Letters).

FILE REACHES SUPERVISION

Final Charging Order is granted after IVA has been approved at a meeting of creditors.

ICO IO(?) MOC FCO

![]()

NOMINEE MOCD SUPS

To find out if McCambridge Duffy can help you regain control over your finances before matters are taken out of your hands, or to find out what kind of debt solution might be right for you, simply get in touch via one of the methods below...

" McCambridge Duffy have been great, completely open, honest and non-judgemental from the first phone call. Kept me fully informed through every stage, always did exactly what they said they would and always got back to me promptly. Fully recommended."

Work out what your new monthly IVA repayment could be by filling in our debt and budget calculator form.

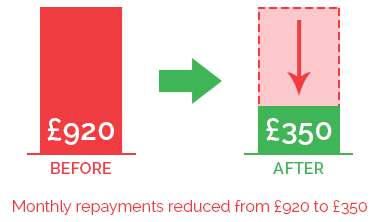

In the IVA example pictured above, our client was struggling with payments of £600 per month to their creditors. We were able to reduce the payment to £240 per month. After 60 months of paying this reduced amount, their IVA will be complete. Any remaining debts will be written off and they will be able to start over debt free.

Chat with one of our debt advisors. We are available to answer any of your questions.

© 2021 McCambridge Duffy Insolvency Practitioners.

All rights reserved

McCambridge Duffy LLP is a Limited Liability Partnership

registered in England and Wales.

Registered number OC309544

Registered office 17 Hanover Square, Mayfair,

London, W1s 1HT