An Individual Voluntary Arrangement (IVA) is a formal debt solution, available in England, Wales and Northern Ireland, that can help you deal your unaffordable unsecured debts, such as credit cards, loans, overdrafts etc...

In an IVA, you propose an affordable repayment plan to your creditors (the people you owe money to), explaining how much you can afford and the reasons why. If they accept your offer, the IVA becomes legally binding for all parties involved and you can begin making your affordable monthly payments as arranged.

You will need the services of a professional called an Insolvency Practioner (IP) to set up and negotiate your IVA proposal with your creditors. They will also facilitate your IVA for it's duration, which is typically 5 years, or 60 months. If you are a homeowner with equity above £10,000 in the property, you may be required to make additional payments into the IVA for another 12 months, meaning the duration of your IVA would be 6 years or 72 months.

On successful completion of the IVA, any remaining debts are legally written off, meaning you can start over with a clean slate.

If you are experiencing financial difficulty and are unable to repay your debts, an IVA could be a suitable solution for you. If you would like to know more about an IVA or any other debt solutions, click the button below to fill in the form. One of our advisors will get in touch and provide advice on your options.

* An IVA may not be suitable in all circumstances. Fees may apply. Your credit rating may be affected.You will firstly be assesed by a debt advisor, to determine if an IVA is your best option. They will run through some questions, review your household income, expenses and debts, with a view to working out how much you can realistically afford to pay towards your debts. They will provide an explanation of all options that you have available and why, including if an IVA is suitable or not. This allows you to make an informed decision on how you would like to deal with your debts.

If you decide to proceed with an IVA, your IP will draft your IVA proposal along with any supporting documentation that you are asked to provide. The proposal will outline how much you can afford to pay each month and explain why the IP thinks it is your best course of action for addressing the debts. The proposal is sent to your creditors to review and vote on. If at least 75% of voting creditors (by debt value), agree to your IVA proposal, then your IVA is accepted and you can begin making the reduced monthly payments towards your debts. You and your creditors will be bound by the terms of the IVA and your creditors cannot take any further action against you when the IVA is accepted.

Your IP will oversee and maintain your IVA for it's lifespan, reviewing everything regularaly and ensuring it remains affordable and fair for all parties involved. They will aim to see it through to successful completion. When you have completed your IVA successfully, your remaining debts are cleared, allowing you to start over debt free.

An IVA may not be suitable for everyone. You must meet the basic criteria in order to be considered. We have outlined some of the main criteria involved in applying for an IVA below:

If you feel like an IVA could be a suitable option for you, please get in touch and we will be happy to assess your situation and advise you on all options. You can also click here to fill in the IVA Calculator on our website and get an idea of what your IVA payment could be, or click here to read our Frequently Asked Questions about an IVA.

PLEASE NOTE: We have a very high IVA acceptance rate. We will only ever put forward an IVA proposal if we believe it is your best option and has a high chance of being accepted by your creditors. We do not charge upfront fees for setting up your proposal, so in the unlikely event that it is rejected by your creditors, you wont have to pay a single thing.

Be aware that some companies charge an upfront fee for creating your IVA proposal. If the proposal is rejected, you could end up out of pocket and in a worse financial position than before.

As with any formal insolvency solution there are both advantages and disadvantages that will apply. You must make sure to consider everything carefully before you enter into this kind of arrangement. We have detailed the main pros and cons below.

STEP 1: When you contact us for debt advice, we will have a chat about your current financial situation, including an assessment of your income, outgoings and your debts. We will let you know all options available for addressing your debts, so that you can have a think about what is the best approach for you.

STEP 2: If you decide that you want to proceed with an IVA, our team will begin working on your IVA proposal. We will only put forward a proposal if we think an IVA is the best solution for you and if the majority of your creditors will accept it. Because of this we have a very high acceptance rate.

Your proposal will state your intention and plan of repayment to your creditors. The repayment structure is normally 60 monthly payments, but you could do a lump sum IVA depending on your circumstances.

STEP 3: Once everything has been agreed with you, a copy of your proposal is sent to the relevant creditors. We then gather their votes to accept or reject the proposal. If your IVA is approved, your payments can begin. We will remain with you at every stage throughout the process, should you need to contact us. All communication with your creditors can be done through us.

NOTE: Anything we discuss is done so in total confidence and is with no obligation.

1: If you are struggling with debt repayments, contact us. We understand that reaching out for debt help is not easy, so we have a handy Online Debt Chat facility on our website, in case you are nervous about speaking on the phone initially. We can also have initial conversations via email if this is something you feel more comfortable with.

2: If you don't think an IVA is right for you, then feel free to contact us for some information on what other options may be available for you; such as Bankruptcy or Debt Management. We will also be happy to signpost you to an apropriate provider or charity if you choose a debt solution that we cannot help with.

Reputation and Experience

Having been in Business for well over 80 years, we are one of the UKs leading IVA Providers. We specialise in both personal and Business IVAs. We have a dedicated team of advisors and In-House Insolvency Practitioners who are well known for their exceptional Customer Service. Click here to see what some of our clients have to say on independent review site TrustPilot, about the service we provide.

High Acceptance Rate

We have an amazing acceptance rate for IVAs proposed. We know any IVAs we propose will have a great chance of being accepted. We also fight very hard for every client to make sure their IVA proposal is carefully considered by the creditors. Our proposals will always be based on something that is affordable and because of this every IVA we propose will be unique.

Customer Service

We have an excellent customer care team. We are a family run company and our advisors have all been with us for many years. They are highly trained and will be able to answer any question quickly and professionally. You will also find us very friendly.

Fast Set Up

We get to work on your case immediately. We usually have an IVA in place within several weeks.

No Upfront Fees

Unlike some of our competitors, we do not charge any upfront fees for putting forward your IVA Proposal. If your IVA application is unsuccessful, you will never receive a bill from us.

1: Everything regarding an IVA and the fees involved is explained fully, before we put any IVA proposal forward. It is free to put forward an IVA proposal with McCambridge Duffy. We do not charge any upfront fees for drafting and submitting your Proposal. In the event that your IVA proposal is unsuccessful, then you will not be charged a penny from us. In saying that, we would only put a case forward if we believe it will be a successful one for both you and your creditors.

2: On successful application of an IVA, fees for managing the arrangement are deducted from your affordable monthly payment (or from your agreed lump sum payment). You will never be asked for additional fees or receive a bill from us. Fees are determined by the creditors (no matter which provider you use).

3: We are the longest established IVA provider in the UK and have thousands of happy clients. We also have one of the highest success rates in the industry.

4: We have 5 full time Insolvency Practitioners in house, giving us a wealth of experience and knowledge. You can read more about our fees and key information by clicking here,

Call us now on 0800 043 3328 for confidential, no obligation IVA advice.

" McCambridge Duffy have been great, completely open, honest and non-judgemental from the first phone call. Kept me fully informed through every stage, always did exactly what they said they would and always got back to me promptly. Fully recommended."

Work out what your new monthly IVA repayment could be by filling in our debt and budget calculator form.

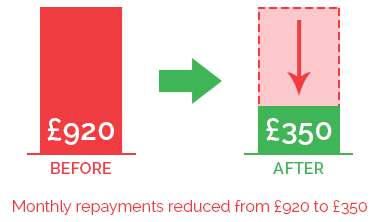

In the IVA example pictured above, our client was struggling with payments of £600 per month to their creditors. We were able to reduce the payment to £240 per month. After 60 months of paying this reduced amount, their IVA will be complete. Any remaining debts will be written off and they will be able to start over debt free.

Chat with one of our debt advisors. We are available to answer any of your questions.

© 2021 McCambridge Duffy Insolvency Practitioners.

All rights reserved

McCambridge Duffy LLP is a Limited Liability Partnership

registered in England and Wales.

Registered number OC309544

Registered office 17 Hanover Square, Mayfair,

London, W1s 1HT