Bankruptcy is a term given to a form of dealing with your debts that you can no longer afford to pay. It enables you to wipe the slate clean in a debt sense, allowing you to start afresh. All your existing assets are taken from you and are divided up and given to your creditors.

Anyone can go Bankrupt; Whether you are self employed, a member of the public, or in a partnership. There are different forms of Bankruptcy for your circumstances.

Bankruptcy occurs when a petition is presented either by yourself (debtors petition) or your creditors (creditors petition). When this is done, the court makes a Bankruptcy order.

The petitions are usually present at your local County Court. In England and Wales it can be presented against you, even if you are not present.

Sometimes government departments start bankruptcy proceedings in the High Court in London or in one of the District Registries. If you did not trade or do not live in the London area, your case will usually be transferred to the appropriate local county court and, if a bankruptcy order is made, it will be dealt with by the local Official Receiver.

Once it has been made, it is advertised in “The London Gazette” (an official publication which contains legal notices) and in a local or national newspaper (or both). In addition the Official Receiver will give written notice of the order to a number of organisations.

There are two people who deal with your case, outlined below:

An Official Receiver is appointed by the Secretary of State and is an officer of the court. Their job is to take charge of administering your bankruptcy and protecting your assets from the date of the bankruptcy order.They will be trustee of your bankruptcy estate unless an insolvency practitioner (IP) is appointed.

They are also responsible for looking into your financial affairs for the period before and during your bankruptcy. They may liase with the court and/or your creditors. The Official Receiver must also report any matters which indicate that you may have committed criminal offences in connection with your bankruptcy or that your behaviour has been dishonest or you have been in some way to blame for your bankruptcy.

Their job is also to give notice of the bankruptcy order to local authorities, utility suppliers, courts, sheriffs, bailiffs, National Savings and Investments (premium bonds), the Land Registry and any relevant professional bodies. Enquiries will also be made of banks; building societies; mortgage, pension and insurance companies; solicitors, landlords and any other persons or organisations who may be able to provide details of any assets or liabilities that you have, or have had, an interest in (either on your own or jointly with others). Third parties will also be asked about any other matters relating to your bankruptcy.

If you are unhappy with the way your case is handled by the Official Receiver you should contact The Insolvency Service to see the complaints procedure. You can research this online.

Insolvency practitioners are people who specialise in Insolvency. They must be authorised by an appropriate professional body. The IP can be trustee instead of the Official Receiver. They are then responsible for disposing of your assets and your payments to your creditors.

If you are unhappy with the way your case is handled by your IP you should contact their recognised professional body.

When a bankruptcy order has been made, you must:

You may also have to go to court and explain why you are in debt. If you do not co-operate, you could be arrested.

*Your books and papers will normally be destroyed after your trustee has finished with them. However, you can have them back, provided they have not already been destroyed, if the court annuls your bankruptcy.

If you are made bankrupt, you must not make payments direct to creditors. Creditors to whom you owe money when you are made bankrupt make a claim to your trustee (that is, either the Official Receiver or an insolvency practitioner). They should not ask you directly for payment; if you receive any requests, pass them immediately to your trustee to deal with and tell the creditor that you are bankrupt.

Suppliers of services to your home (gas, electricity, water and telephone) may not demand from you payment of bills in your name which are unpaid at the date of the bankruptcy order. But they may ask you for a deposit towards payment for further supplies or could arrange for the accounts to be transferred into the name of your spouse or partner. You must pay continuing commitments such as rent (if you rent your home), together with any debts you incur after the bankruptcy.

The Official Receiver/IP will tell your creditors that you are bankrupt. He or she may either act as the trustee or may arrange a meeting of creditors for them to choose an insolvency practitioner to be the trustee. This happens if you appear to have significant assets. You may have to attend the meeting.

The trustee will tell the creditors how much money will be shared out in the bankruptcy. Creditors then have to make their formal claims. The costs of the bankruptcy proceedings are paid first. The costs include fees that the Official Receiver or the insolvency practitioner charge for handling your case.

If applicable, claims from your employees are next in line to be paid, along with any other preferential debts. Finally, other creditors are paid, together with interest on all debts, as far as there are funds available from your assets. If there is a surplus, it will be returned to you. You would then be able to apply to the court to have your bankruptcy ‘annulled’ (cancelled).

When your trustee makes a payment to your creditors, he may place an advertisement about your bankruptcy in a newspaper asking creditors to submit their claims. Depending on how long it takes your trustee to deal with your assets, this advertisement may appear several years after the bankruptcy order.

You no longer have any control over your assets.

You can keep the following items unless their individual value is more than the cost of a reasonable replacement:

All these items must be disclosed to the Official Receiver/IP who decide if you can keep them or not.

If you have made a claim against another person through court proceedings, or you think you may have a claim (a right of action) against another person, the claim may be an asset in the bankruptcy.

If you own your home, whether freehold or leasehold, solely or jointly, mortgaged or otherwise, your interest in the home will form part of your estate which will be dealt with by your trustee. If you own it, or are paying a mortgage, the house may have to be sold to go towards paying your debts.

If your husband, wife or children are living with you, it may be possible for the sale in the bankruptcy to be put off until after the end of the first year of your bankruptcy. This gives time for other housing arrangements to be made. Your husband, wife, partner, a relative or friend may be able to buy your interest in your home from the trustee. This may be so even if that interest is very small, worth nothing or you owe more on the house than it is currently worth. Such a purchase would prevent a sale of the property by the trustee at a future date. Your spouse or any other interested party should be encouraged to take legal advice about the home as soon as possible.

If the trustee cannot, for the time being, sell your home, he or she may obtain a charging order on your interest in it, but only if that interest is worth more than £1,000. If a charging order is obtained, your interest in the property will be returned to you, but the legal charge over your interest will remain. The amount covered by the legal charge will be the total value of your interest in the property and this sum must be paid from your share of the proceeds when you sell the property.

Until your interest in the home is sold, or until the trustee obtains a charging order over it, that interest will continue to belong to the trustee but only for a certain period, usually 3 years, and will include any increase in its value. Therefore, the benefit of any increase in value will go to the trustee to pay your debts, even if the home is sold some time after you have been discharged from bankruptcy.

If, after a certain time, usually 3 years, your trustee has not sold or obtained a charge over your interest in the property, or applied for an order of possession or obtained a charging order against the property, or you have not come to any arrangement with your trustee about that interest, it may be returned to you.

A trustee cannot usually claim a pension as an asset if your bankruptcy petition was presented on or after 29 May 2000, as long as the pension scheme has been approved by HM Revenue and Customs.

For petitions presented before 29 May 2000, trustees can claim some kinds of pensions. A separate publication called “What will happen to my pension?” is available from your local Official Receiver’s office or The Insolvency Service Publications Order Line (address on back cover).

If you are receiving a pension or become entitled to do so before you are discharged, the pension is included as income for the purposes of an income payments order (IPO).

Generally, your trustee will be able to claim any interest that you have in a life assurance policy. The trustee may be entitled to sell or surrender the policy and collect any proceeds on behalf of your creditors. If the life assurance policy is held in joint names, for instance with your husband or wife, that other person is likely to have an interest in the policy and should contact the trustee immediately to discuss how their interest in the policy should be dealt with.

You may want the policy to be kept going. Ask your trustee: it may be possible for your interest to be transferred for an amount equivalent to the present value of that interest.

If the life assurance policy has been legally charged to any person, for instance an endowment policy used as security for the mortgage on your home, the rights of the secured creditor will not be affected by the making of the bankruptcy order. But any remaining value in the policy may belong to your trustee.

Any registration, licence or permission you hold in connection with your work or trade might be affected by the making of the bankruptcy order. You should inform the person who issued the registration or authority of your bankruptcy to establish if it will remain in force or will be cancelled or withdrawn. Any value attaching to these items may belong to the trustee. In considering this issue you should disregard items of a personal nature such as a driving licence.

If you are self-employed, your business is normally closed down and any employees are dismissed. Any business assets will be claimed by the trustee unless they are exempt and you will have to give the Official Receiver all your accounting records. You are still responsible for completing all tax and VAT returns. Your employees may be able to make a claim to the National Insurance Fund for outstanding wages and holiday pay, payment in lieu of notice, and redundancy. Employees can claim in the bankruptcy for any money owed that is not paid by the National Insurance Fund.

For further details, you should contact the Redundancy Payments Service on 0845 145 0004.

There is nothing to prevent a bankrupt from being self-employed. So you can start to trade again, subject to restrictions. You will be responsible for keeping accounting records for this business and for dealing with the tax and VAT requirements for the new business. You will need to register again for VAT if you meet the registration requirements. You should not continue to use your pre-bankruptcy VAT registration number.

Your trustee may apply to court for an income payments order (IPO), which requires you to make contributions towards the bankruptcy debts from your income. The court will not make an IPO if it would leave you without enough income to meet the reasonable domestic needs of you and your family. If you have an increase or decrease in income, the IPO can be changed.

IPO payments continue for a maximum of 3 years from the date the order is made by the court and may continue after you have been discharged from your bankruptcy. Or you may enter into a written agreement with your trustee, called an income payments agreement (IPA), to pay a certain amount of your income to the trustee for an agreed period, which cannot be longer than 3 years. There are no fixed guidelines on IPOs or IPAs - each case is assessed individually.

The following are criminal offences for an undischarged bankrupt:

You may not hold certain public offices. You may not hold office as a trustee of a charity or a pension fund.

After the bankruptcy order, you may open a new bank or building society account but you should tell them you are bankrupt; they may impose conditions and limitations. You should ensure you do not obtain overdraft facilities without informing the bank that you are bankrupt, or write cheques which are likely to be dishonoured. Tell your trustee about any money that you have in the account which is more than you need for your reasonable living expenses. Your trustee can claim the surplus amounts to pay your creditors.

If you were made bankrupt on or after 1 April 2004, you will be automatically freed from bankruptcy (known as “discharged”) after a maximum of 12 months. This period may be shorter if the Official Receiver/IP concludes his enquiries into your affairs and files a notice in court.

If this is your first bankruptcy, you will be discharged automatically on 1 April 2005 or, if you currently expect your discharge date to be before 1 April 2005, you will receive your discharge on that earlier date.

If you have been an undischarged bankrupt at any time during the 15 years before the current bankruptcy (unless the previous bankruptcy has been annulled) you will be discharged automatically on 1 April 2009. Or you may ask the court for a discharge 5 years after the date of the bankruptcy order, but the court may refuse or delay your discharge, or grant it conditionally on terms requiring you to make some payments out of your income.

You will also become free from bankruptcy immediately if the court annuls (cancels) the bankruptcy order; this would normally happen when your debts and the fees and expenses of the bankruptcy proceedings have been paid in full or the bankruptcy order should not have been made.

On the other hand, if you have not carried out your duties under the bankruptcy proceedings, the Official Receiver may apply to the court for your discharge to be postponed. If the court agrees, your bankruptcy will only end when the suspension has been lifted and the time remaining on your bankruptcy period has run. If your discharge has been suspended (stopped) prior to 1 April 2004, you should contact the Official Receiver for information about how and when you may be discharged from bankruptcy.

Discharge releases you from most of the debts you owed at the date of the bankruptcy order. Exceptions include debts arising from fraud and any claims which cannot be made in the bankruptcy itself. You will only be released from a liability to pay damages for personal injuries to any person if the court thinks fit.

When you are discharged you can borrow money or carry on business without the restrictions previously referred to. You can act as a limited company director unless you are disqualified from doing so as a result of a separate order arising out of your involvement with a company.

When you are discharged there may still be assets that you owned, either when your bankruptcy began, or which you obtained before your discharge, which the trustee has not yet dealt with. Examples of these may be the interest in your home, an assurance policy or an inheritance. These assets are still controlled by the trustee who can deal with them at any time in the future. This may not be for a number of years after your discharge.

With some assets - such as your home and some types of assurance policy - your spouse, a partner, a relative or friend may want to buy your interest. He or she should get in touch with the trustee straightaway to find out how much they would have to pay.

You must tell the Official Receiver about assets you obtain after the trustee has finished dealing with your case but before you are discharged. These assets could be claimed to pay your creditors. You have a duty to continue to assist your trustee after you have been discharged.

Usually you may keep all assets you acquire after your discharge.

If, during his/her enquiries into your affairs, the Official Receiver decides that you have been dishonest either before or during the bankruptcy or that you are otherwise to blame for your position, he/she may apply to the court for a bankruptcy restrictions order. The court may make an order against you for between 2 and 15 years and this order will mean that you continue to be subject to the restrictions of bankruptcy. You may give a bankruptcy restrictions undertaking which will have the same effect as an order, but will mean that the matter does not go to court.

Bankruptcy deals with your debts at the date of the bankruptcy order. After that date you should manage your finances more carefully. If you incur new debts this could result in:

To find out if McCambridge Duffy can help you regain control over your finances before matters are taken out of your hands, or to find out what kind of debt solution might be right for you, simply get in touch via one of the methods below...

" From the moment we contacted McCambride Duffy we were reassured by professional staff who knew what they were doing. If we had any questions or concerns, a quick phone call was all it took to sort things out. We are completely satisfied with the service we have received and would recommend Mccambridge Duffy to anyone who is having financial problems. "

Work out what your new monthly debt repayment could be by filling in our debt and budget calculator form.

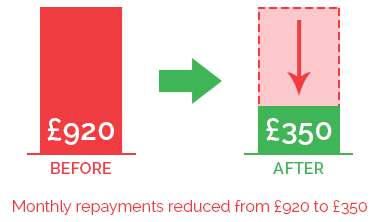

Client was paying over £920 per month to creditors. We were able to have this reduced to £350 per month, with all interest and charges frozen. After 60 months of paying this reduced amount their solution was complete, their remaining debt was written off and they were free of their debts.

Chat online with one of our debt advisors. We are available now to answer any of your questions.

© 2021 McCambridge Duffy Insolvency Practitioners.

All rights reserved

McCambridge Duffy LLP is a Limited Liability Partnership

registered in England and Wales.

Registered number OC309544

Registered office 17 Hanover Square, Mayfair,

London, W1s 1HT