| Endowment | ISA | Adverse Credit Mortgage |

|---|---|---|

|

|

|

Is the Current Mortgage up-to-date?

Effect of Arrears on Ability to Remortgage

Income/Affordability

Self-Certified Mortgages

Examples of Adverse Lenders

Secured Loans

Early Redemption Penalties

Remortgage Example 1 - Remortgage for a one off IVA

Proposed value of house: £120k

Mortgage outstanding on house: £80k

Debts outstanding of £80k

Remortgage of £28k to go as full and final settlement towards the debt outstanding.

Remortgage Example 1 - Remortgage for a one off IVA

Proposed value of house: £120k

Mortgage outstanding on house: £70k

Debts outstanding: £80k unsecured debt

One off IVA @ 90% loan to value £108,000

Less £70k mortgage – leaves £38k for one off IVA

There are several debt solutions available that can help you deal with unaffordable debt, that do not involve you having to remortgage your house. If you are a homeowner and struggling with debt repayments and would like to know your options, please get in touch. We offer free, confidential no obligation advice. Fill in the form below to get some advice.

" McCambridge Duffy have been great, completely open, honest and non-judgemental from the first phone call. Kept me fully informed through every stage, always did exactly what they said they would and always got back to me promptly. Fully recommended."

Work out what your new monthly IVA repayment could be by filling in our debt and budget calculator form.

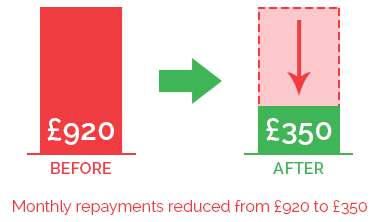

In the IVA example pictured above, our client was struggling with payments of £600 per month to their creditors. We were able to reduce the payment to £240 per month. After 60 months of paying this reduced amount, their IVA will be complete. Any remaining debts will be written off and they will be able to start over debt free.

Chat with one of our debt advisors. We are available to answer any of your questions.

© 2021 McCambridge Duffy Insolvency Practitioners.

All rights reserved

McCambridge Duffy LLP is a Limited Liability Partnership

registered in England and Wales.

Registered number OC309544

Registered office 17 Hanover Square, Mayfair,

London, W1s 1HT