When a company borrows money from a bank on an overdraft or loan, it will be common for the bank to ask for a security (debenture) against such a loan. If anything goes wrong with the business this security gives the bank more power to get their money out of the company. Essentially it is like a secured loan or a mortgage on your house. If the company runs into financial difficulty then the bank can call the money in more easily than without the security.

Before September 2003 this used to be a very common debt recovery tool for the banks. On 15th September 2003 the UK Government introduced changes, set out in the Enterprise Act 2002, to phase out Receivership as a debt solution. The reason for this is that the banks were usually first to be aware of a company's financial worries and made sure they got their money out quickly without any consideration for the other creditors.

It is less commonly used now and will disappear gradually. Most often banks use administration as a solution now.

Note: If your company has borrowed money from a bank before 15th September 2003 and you granted a debenture (security) before that date, then it is still possible for the bank to appoint a receiver. If the borrowing was after that date they cannot appoint a receiver at all.

The Receiver's role is mainly concerned with getting back any money owed to the bank. The Receiver may sell the business as a whole or sell assets individually, to pay off the bank, and the costs of the receivership, which are usually quite high.

Preferential creditors may see their debts repaid by the receiver.

From the company's point of view the company is rarely saved in its existing form, its assets will be subject to "meltdown", often jobs and economic activity are lost.

From the directors' perspective he/she will typically lose their employment and any monies the company is due to them and the company may cease to trade. In addition the director's conduct may be investigated.

From the creditors' perspective it is unlikely that any unsecured creditors will receive any of their money back and often they lose a valuable customer. The cost of receivership can be very high and the bank has to pay the receiver's costs.

" I found McCambridge Duffy to deliver on what they said they would do and to do so quickly with a minimum of fuss. There were not endless phone calls and letters but they got the facts, assembled the proposal and put it in place very quickly. The process was made less stressful by the way in which they managed it."

Work out what your new monthly debt repayment could be by filling in our debt and budget calculator form.

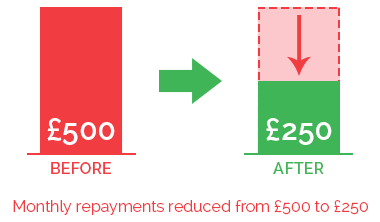

Client was struggling with monthly debt repayments of £500 to several creditors. We were able to have this reduced to £250 per month, with all interest and charges frozen. In 60 months, any remaining debts will be written off and they will be debt free.

Chat online with one of our debt advisors. We are available now to answer any of your questions.

© 2021 McCambridge Duffy Insolvency Practitioners.

All rights reserved

McCambridge Duffy LLP is a Limited Liability Partnership

registered in England and Wales.

Registered number OC309544

Registered office 17 Hanover Square, Mayfair,

London, W1s 1HT