Click on the links below to find answers to your questions. If you cannot see the question you are looking for, simply fill in the form on this page and an advisor will call you to discuss your query.

A Protected Trust Deed (PTD) enables you to make a formal proposal for payment to your creditors through an Insolvency Practitioner. The proposed payments will be less than the full amount of the debt owed but your creditors would be accepting the offer in full and final settlement of their claim.

Your creditors have the right to vote whether to accept or reject your proposal but were they vote to accept it, a legal agreement is created which is binding on you and your creditors. The proposal will be tailored to meet your individual circumstances but typically would involve you paying a monthly payment, a lump sum or some combination of the two. When you sign a Trust Deed your assets are transferred to the nominated Insolvency Practitioner, who becomes your Trustee. Any valuable assests would be sold to help pay your creditors, but you are able to keep most of the things you need for day-to-day living. Proposals can also take account of eratic income such as overtime or bonuses.

If your creditors are hassling you and there is no light at the end of the tunnel with regards to paying off your debts, or if you feel you will be paying them off for eternity then a Trust Deed may be extremely beneficial.

One of the best things a Trust Deed can offer you is a guaranteed date when your payments will stop and your debt will be cleared, which is usually three years. If you can be guaranteed an end to the problem then the future will be a lot brighter.

Other benefits of Trust Deeds are:

No, you will not have to go to court.

No. The Trustee must place a notice in a legal newspaper called the Edinburgh Gazette. This paper cannot be purchased on the high street. It is specifically designed for financial institutions (banks, building societies etc...), Insolvency Practitioners etc...

No. But it is usually recommended that you inform your partner. If debts are in joint names then your partner would have to be informed.

From the date of publication of the notice in the Edinburgh Gazette your creditors have a period of 5 weeks within which they must submit a rejection to us in writing.

The Trustee will not contact your creditors until you are granted a Trust Deed. However, you should notify them you are taking professional advice about it.

If more than one third in value or a majority in number of your creditors place a notice of objection with the Trustee before the 5 week deadline then the Trust Deed cannot become protected.

The Trustee will assist you in applying to the Court for an Award of Sequestration which the creditors have to accept.

The Trust Deed does not cut down a wages arrestment that is in place prior to the Trust Deed. However, most creditors will cancel this after the Trust Deed is protected.

Only if you have debt with that particular bank it is recommended.

No. The only way they can find out is from the Edinburgh Gazette or if a creditor notifies them.

The Trustee has to comply with Money Laundering Regulations and Proceeds of Crime legislation and confirm your identity. This also applies to any third party who may provide funds on your behalf unless paid through a solicitor who is required to undertake his own checks.

The Trustee places an Inhibition as a security over the property so that this cannot be sold or further borrowing arranged without trustee consent.

This will be removed once the payment agreement is completed and all asset values have been dealt with and the trust deed is concluded.

Can be arranged at any time during Trust Deed period but as early as possible preferable. Can be arranged in part at commencement and again after 3rd anniversary to deal with any balance.

This must be continued to be paid or your home is at risk.

The mortgage and any securities attached to the property will be settled and residual balance will be forwarded to trustee subject to relocation allowance. Normally up to £1,000 per owner.

Yes we can put you in touch with an Independant Financial Advisor (IFA) who can assist people in Trust Deed arrangements or you may appoint your own.

The Trustee has no interest unless your partner has also granted a Trust Deed.

Yes. You have to inform the lender that you are in a PTD and it is the finance company's decision. The Trustee wil not normally consent if the monthly cost is higher as it cannot affect your Trust Deed payments.

Yes, as long as this is for travel to work purposes and monthly payments are being maintained with the consent of a finance company holding a security over the vehicle.

To determine equity value if over £1,000 at completion of payment agreement.

Not usually, as the Trustee will provide consent if needed and as long as monthly contributions are paid to your Trust Deed.

If you wish to retain the policy you have to pay the cash surrender value to retain this. A third party payment can be accepted or the Trust Deed extended after the 3rd anniversary. Alternatively the policy can be surrendered with your share of the value paid to the Trustee.

The Trustee must collect the value of all investments you hold either through a sale or by extending the period of your Trust Deed to collect additional payments. Third party payments can also be accepted.

Your creditors have no direct claim against your pension fund however your Trustee must assess your ability to pay monthly contributions from all your sources of income including pension benefits.

Your debts are often transferred to debt collecting companies who may try and make you pay. However it is illegal for you to make any payment to your creditors after you have granted a Trust Deed.

This means a Court Judgement has been made against you and you or the creditor can apply for your affairs to be sequestrated i.e. made formally bankrupt.

The dividend payment will be made to the new owner and not the original creditor and the balance is legally written off.

No it will grant the creditor a form of security if in place prior to the Trust Deed.

These are assessed on two thirds of your disposable income subject to a minimum payment of £250 per month over a three year period.

If your disposable income is increased through extra income or savings in essential expenditure then the Trustee will request a higher amount each month based on your ability to pay.

The total joint income needs to be taken to establish your share of joint household expenditure on a pro rata basis.

There has to be a valid reason for this with medical proof needed if caused by serious illness. If non co-operation then the Trustee may arrange for your affairs to be sequestrated (formal bankruptcy).

The Trustee can normally accept a lump sum to complete your payment agreement at any time. The source of funds will need to be verified.

Notify Trustee who will require details of any redundancy and severance payments. If only temporary then Trustee can suspend monthly payments until you resume work again.

The Trustee will obtain a copy of the death certificate and examine if any Will prepared. Creditors are entitled to benefit from any funds arising.

You must inform the Trustee and provide full details as your Trust Deed creditors are entitled to benefit from this.

No discharge certificate just a letter advising completion of trust deed and what has been paid to your creditors.

There is no requirement to attend.

It is up to the individual creditor whether they update your credit file, and the credit rating can take from 6 to 15 years from the end of the trust deed. The Trustee has no responsibility for this.

If you need help with paying your debts, simply get in touch with us on 0800 043 3328 or contact us by filling in a form and we will get in touch with you..

" McCambridge Duffy have been great, completely open, honest and non-judgemental from the first phone call. Kept me fully informed through every stage, always did exactly what they said they would and always got back to me promptly. Fully recommended."

Work out what your new monthly IVA repayment could be by filling in our debt and budget calculator form.

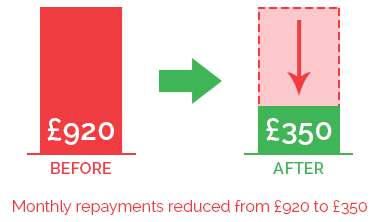

In the IVA example pictured above, our client was struggling with payments of £600 per month to their creditors. We were able to reduce the payment to £240 per month. After 60 months of paying this reduced amount, their IVA will be complete. Any remaining debts will be written off and they will be able to start over debt free.

Chat with one of our debt advisors. We are available to answer any of your questions.

© 2021 McCambridge Duffy Insolvency Practitioners.

All rights reserved

McCambridge Duffy LLP is a Limited Liability Partnership

registered in England and Wales.

Registered number OC309544

Registered office 17 Hanover Square, Mayfair,

London, W1s 1HT