When you apply for an IVA, your Insolvency Practitioner (IP) drafts a proposal explaining how much you can afford to pay towards your debts and why. Your creditors are invited to vote in favour of, or against your proposal in a Meeting of Creditors.

For an IVA to be approved, at least 75% of your voting creditors (by debt value) must agree to the proposal. If your IVA proposal is accepted, then you can begin your IVA repayments as arranged. Some creditors may propose some modifications to the proposal in order, which must be agreed to and accepted before they vote.

If less than 75% of your creditors (by debt value) vote in favour of your proposal or if creditors vote against your IVA proposal, your IVA is rejected. The most common cause of rejection of an IVA proposal is when your creditors do not believe that the proposed repayment plan is enough to meet individual creditor guidelines.

If you have applied for an IVA and creditors have rejected it, you will still have options for dealing with your unaffordable debts.

In some instances, you might be able to submit a new IVA application. We can assess your rejected IVA proposal, analyse the objections raised by creditors, including their reasons why, and explore the potential for submitting a revised IVA proposal.

If you are unable to propose another IVA, there may be some alternative options available for you, such as a Debt Management Plan, a Debt Relief Order or Bankruptcy. We can help you explore all possible options.

If your IVA has been rejected and you would like to have a chat with one of our advisors to find out your options, click the link below and fill in the form or call us on 0800 043 3328.

Click here to discuss a rejected IVA with one of our advisors

Here at McCambridge Duffy, we have a very high success rate with having IVAs approved. This is because we do not put forward an IVA unless we believe it will be a successful one for all parties involved. If, for any reason your IVA propsal is rejected, it may be possible for your IP to re-negotiate the proposal with your creditors, providing you are in a position to offer a revised IVA payment and agree to the revised terms. If you cannot agree to a revised IVA propsal, then you will need to look at other ways of addressing your debt problems. We can discuss other options available to you.

Make sure you are applying for an IVA with the help of a trusted IVA Provider. Any respectable IVA company will only put through a proposal on your behalf if it adheres to recommended guidelines and is fair for both you and your creditors. This will increase your chances of having it approved successfully.

An Insolvency Practitioner should not recommend an IVA to you unless it is your most suitable option for dealing with your debt.

Do not pay any upfront fees for making an IVA proposal. In the event that it might fail, you will lose any upfront payments you have made.

If your IVA has been rejected at a meeting of creditors it may be possible to re-propose an IVA if you are in a position to offer an alternative level of debt repayment. If you feel that this is the case please contact us online or on 0800 043 3328 to discuss your options.

However, it could be that an IVA may not be the best possible solution for your financial problem. There are alternatives to IVA’s which may suit your individual circumstances better. A brief explanation of each of these solutions is listed below

A Debt Management Plan (DMP) is an informal arrangement with your creditors, where you agree to repay your debts with reduced affordable monthly payments. The plan will last as long as it takes for you to pay your debts in full, or until you decide you no longer need to make reduced payments.

If you use the services of a Debt Management Company to set up and facilitate your DMP, you will no longer need to worry about dealing with your creditors, as they will deal with all creditor correspondence on your behalf. They will also try to negotiate a freeze on all interest and charges during your DMP, but this cannot be guaranteed as it is not a legally binding arrangement. Your credit rating would be affected as you are not making your usual contractual repayments.

With Debt Consolidation, you can consolidate your debt into one monthly payment by taking out a personal or secured loan. You can use the loan to pay off your current debt in full, and make repayments towards the loan, effectively leaving you with one payment each month. A loan would not be advisable unless you are confident you can keep up with repayments.

Bankruptcy is a legal procedure that is often considered as a last resort debt solution, when you are unable to pay your debts.

You can either apply online for Bankruptcy yourself, or any creditor that is owed more than £5,000 from you, can apply for you to be made bankrupt. There are costs and fees associated with a Bankruptcy application:

- For residents of England and Wales, the costs are about £680.

- For Northern Ireland, the costs are about £683

A Debt Relief Order ( DRO) is sometimes referred to as a cheaper form of 'Mini -Bankruptcy', suitable for people with minimal assets, and very little money left over each month to pay towards their debts. This solution is only available to residents in England, Wales and Northern Ireland currently. The criteria is slightly different for each region, outlined below.

DRO criteria for England and Wales

Your debts must be no higher than £30,000

Assets cannot be more than £2,000

If you own a car, it's value must be under £2,000

Your *disposable income is less than £75 per month

*disposable income is the amount of money you have left over each month after all expenses have been paid.DRO criteria for Northern Ireland

- Your debts must be no higher than £20,000

- Assets cannot be more than £1,000

- If you own a car, it's value must be under £1,000

- Your disposable income is less than £50 per month

You can only apply for a DRO via an approved intermediary. There is a fee of £90 to apply, which you can pay in full or in instalments.

Should you wish to discuss your options click here to fill in the form on this page and one of our advisors will get in touch.

Read some testimonials below to see what some of our clients have to say about the services we offer at McCambridge Duffy. All reviews are collected on Independent review site TrustPilot.

" McCambridge Duffy have been great, completely open, honest and non-judgemental from the first phone call. Kept me fully informed through every stage, always did exactly what they said they would and always got back to me promptly. Fully recommended."

Work out what your new monthly IVA repayment could be by filling in our debt and budget calculator form.

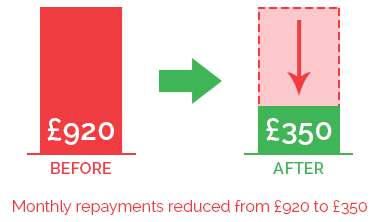

In the IVA example pictured above, our client was struggling with payments of £600 per month to their creditors. We were able to reduce the payment to £240 per month. After 60 months of paying this reduced amount, their IVA will be complete. Any remaining debts will be written off and they will be able to start over debt free.

Chat online with one of our debt advisors. We are available now to answer any of your questions.

© 2021 McCambridge Duffy Insolvency Practitioners.

All rights reserved

McCambridge Duffy LLP is a Limited Liability Partnership

registered in England and Wales.

Registered number OC309544

Registered office 17 Hanover Square, Mayfair,

London, W1s 1HT